HVAC

Years before my interest in consolidation and the start of this Substack, I was told a small nugget of information. A friend in the HVAC business mentioned how some residential HVAC firms in the Des Moines area which had been locally owned were now backed by private equity. This nugget sat in the back of my head until now. While this might seem innocent with private equity owning HVAC companies, this could lead to a rollup of HVAC firms and could potentially lead to higher prices and worse customer service in the years to come.

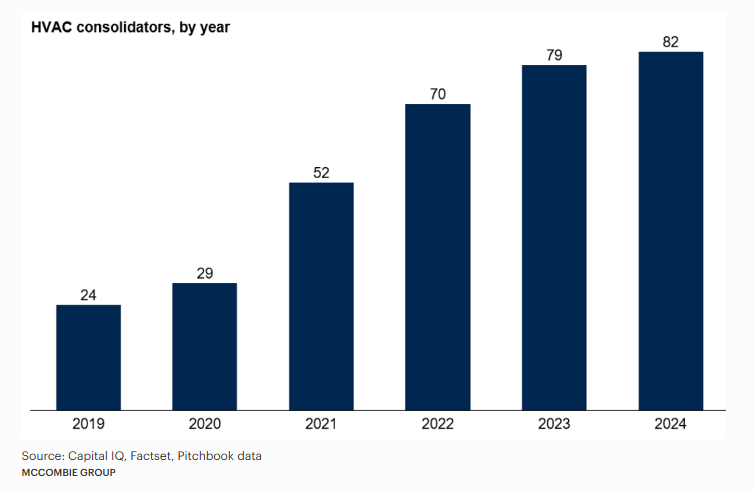

The state of private equity influence and consolidation in the residential HVAC industry is not at alarming levels like the machinery or egg but like the bowling industry. It makes sense for private equity to want to enter the residential HVAC industry. According to Forbes, this merger and acquisition trend has grown considerably in recent years. HVAC consolidators have tripled between 2019 and 2024. With being recession-resistant, an essential service, a fragmented market with consolidation opportunities, and growth tailwinds, it makes sense why this industry is experiencing consolidation.

According to Forbes, “Most PE firms pursue a consolidation or rollup strategy. This involves using a platform company to buy and integrate smaller add-on acquisitions to quickly achieve scale. Of course, growth can be generated through opening up new cities. However, it takes significant time and investment to build brand recognition in a new area from scratch—given their short holding periods, PE generally prefers to acquire proven preexisting businesses. Upon exit, the consolidated entity captures the spread between the higher valuation multiples that larger businesses command and the lower multiples paid for the smaller purchases.”

According to Conduit Tech, investors look to seek repeat revenue (i.e. getting the HVAC system serviced every so often), barriers to entry, ability to consolidate back office operations, and a highly diversified customer base. By consolidating back office operations, this loss of worker power leads to less wealth staying in the community. When private equity decides to combine all the companies under one hat, they can gain monopoly power like having the ability to set prices like the grain processors.

Here is the impact of the nugget. When looking at Schall, Bell Brothers, and Greens, there is no reference to being private equity backed. To add to this onion like deception, there is another layer to peel back. This private equity group owns Turnpoint, which is the company that these three HVAC firms fall under. To the best of my knowledge and research, I am unable to determine if these companies are majority or minority owned by private equity1. Whether they are majority or minority owned, the Turnpoint brand page says each business has a brand leader and not an owner. It is clear Turnpoint wants to appear as the owner of these HVAC companies.

What is disappointing is it is hard for a commoner to realize what firms are private equity backed. Despite this nugget, it took until I found this Reddit to know what firms to look at. The responder to this post is wrong. While Turnpoint supports these businesses, the ultimate owner is a private equity group. If it makes sense to roll up businesses and take them over to potentially sell them in the future, private equity will do that. This is still not a monopoly of the Des Moines market because plenty of other residential firms exist2.

Another interesting piece of the puzzle is a West Des Moines private equity group has also gotten in on the HVAC industry. While still private equity and who knows where their investors live, at least they are based in Iowa. Like the other three firms, Dorrian Heating & Cooling and Heartland Heating & Cooling do not overtly mention being owned by a private equity group. This businesses might not be majority but only minority owned, but the private equity group has talked about it.

This nugget is a terrible secret within the industry. A locally owned HVAC company has a spot on their website dedicated to spotting the differences between locally owned and private equity. This part was fascinating, “One way private-equity HVAC companies try to earn business is through “free,” one-time offers, often seeming too good to be true. If you’re promised a free furnace with the purchase of an air conditioner, for example, the fees you’re paying for the A/C unit are probably marked up significantly. Meanwhile, your supposedly “free” furnace is a cheap model that will need service and replacement much sooner than a high-quality unit would, exposing you to higher costs down the line. Instead of gimmicks, look for companies that reward customer loyalty through rewards programs that prioritize maximizing the lifespan of your HVAC system through routine maintenance and tune-ups.” This is what Schall has done.

This private equity and consolidation trend is also happening across the nation. Look at Turnpoint’s map, they are in many of the United States. An even larger player in this market is Apex Service Partners, who is owned by Alpine Investors. On Apex’s website, they mention about being in fifty of the largest fifty markets in the country and 45 of 50 states. Unfortunately, it is hard to know who they own because they do not list their brands or a map like Turnpoint.

Alpine Investors has also gotten involved in the commercial HVAC business under a different name, Orion Services Group. This has led to them owning in some capacity the Des Moine based Marick Mechanical.

Alpine Investors is making a big bet in this space. The Wall Street Journal interviewed the founder of Alpine Investors. While he said the technicians got a 20% pay bump after a company is sold to Alpine through higher wages, bonuses, and commission, other workers said when private equity bought up their companies, new systems are pushed on customers instead of fixing what is not working. Posters on online forums also said this makes sales less satisfying than doing real repair work.

This path towards consolidation can lead to higher prices, worst customer service, and more wealth leaving the local communities. While this is an example of what is happening in the Des Moines market, there could be impacts on rural Iowa. As private equity groups look to roll up more HVAC businesses and maybe rural Iowa HVAC businesses, they might not see the value in being in lower income rural and urban Iowa. This could create an HVAC desert like the food or health care deserts.

Private equity is not always an evil force, and there can be advantages. It is important to be cautious of these firms when they enter any industry. They are in the business of making money for their investors and not necessarily the community. It is important to be aware of what businesses are locally owned versus private equity owned. If I had never received this small nugget of information, these companies could have maintained their mystique of not being backed by private equity.

I wish I had time to call everyone up, but life happens.